Guiding Questions

Q1: What is the cost of making or not making a sustainability transformation?

Q2: How can corporates leverage their finance capabilities for the transformation?

Q3: How can sustainability issues that will impact the business or operations be identified?

Not a single day passes without pre-warnings from climate change, be it bush fires in Greece, drought in France and Spain, or record-breaking global water temperatures. The visibility of climate change’s consequences is increasing at a significant pace. But so too is the recognition that these fundamental changes come at a cost for both industry and society. Corporates seemingly face two options: paying the price for today’s counteractions or paying a much higher price tomorrow for catching up with a missed sustainability transformation. In this article, we argue why systematically balancing the cost and value implications of a sustainability transformation must be a key topic on each CFO’s agenda.

The sustainability transformation will hit those not prepared

Quantifying the financial impact from (not) making a sustainability transformation is a big challenge for CFOs. As future regulations remain uncertain and exploitation of Earth’s resources still seem to be unlimited, giving up on non-sustainable but profitable business models is hard to argue against pre-existing shareholder interests. Still, ESG-oriented shareholders and investors are not only focused on ethical and moral objectives, but more importantly on the need to develop resilient and — in the long term — value-creating business models. Prominent examples like Exxon Mobil or RWE show such a transformation induced by ESG-oriented investors and refrain from CO2-intense activities. By doing so, they achieve a positive effect in their discounted cash flow model with the help of carbon management and trading.

It is definitely too late to act when an industry sector gets disrupted, and the impact of an unsustainable business model is felt in the company's financial situation. This can currently be observed in the electrification of the automotive industry, the sudden drop in the price of clean energy technologies, the global shocks triggered by the Ukraine war, and the Covid-19 quarantine shutdown. Now is the right time to reconsider business models resting on high carbon emissions. This must be the perspective for CFOs to consider their current strategic and capital allocation decisions. Interestingly, we find the costs of (not) transforming to be predictable. Taking again the CO2 example, the global temperature increase must be limited to 1.5 °C, as the consequences of exceeding this threshold will be devastating. Thus, economic experts in this scientific field agree that introducing a universal carbon price will become mandatory within the next ten years. Given some uncertainty about the timing of the cost implications of carbon emissions, the implications for the competitiveness of the current business model can already be considered today. As regulators will favor market mechanisms to set in and have carbon emissions regulated via pricing, a CFO can now already calculate ten years in the future how costly their operations will become.

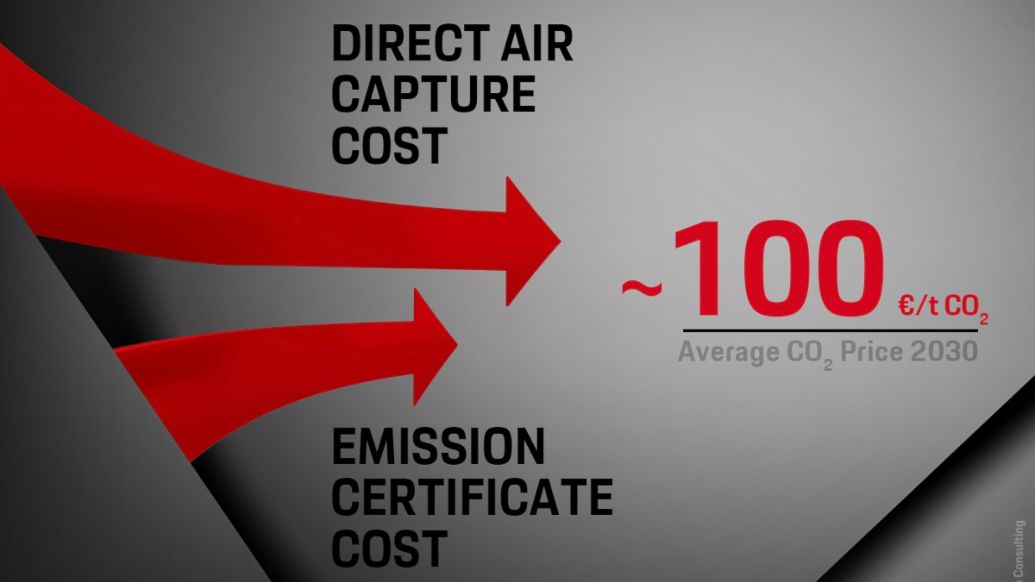

Taking the average price expectation of CO2 till 2030 of €80 to100/t CO2, a financial model gives a good indication of the scope of the strategic and sustainable transformation that is required. While the carbon price levels off, the cost of carbon removal via direct air capture will drop significantly to €100/tCO2 in 2030. As of today, the carbon emission certificate trading markets (ETS) show a CO2 price of slightly above €90/tCO2. Consequently, and even if the German climate targets for 2030 of 438 million metric tons of CO2 are achieved, the expected average CO2 price in the EU will add up to an €88 billion annual cost for German industry as a whole.

The ESG view on a corporate sustainability transformation

Rising CO2 costs make it evident that companies face new cost factors from the sustainability transformation. In order to give CFOs the ability to argue for or against potential business transformations and risks, it becomes necessary to link sustainability issues to business operations via quantified ESG KPIs. Such a link provides a basis for decision-making by quantifying the expected costs compared to the opportunity costs.

Such an approach to ESG management means that the management of financially relevant ESG issues is carried out in an integrated manner together with classic financial topics. One example refers to shadow prices to determine hypothetical cost or internal carbon fees to charge business units individually for every tonne of CO2. If applied properly, it can impact decisions on product design, sourcing, energy procurement, or the use of recyclable raw materials.

In order to leverage this, it must be ensured that relevant ESG topics are integrated into controlling. This enables strategic and operational control as well as company-wide ESG data intelligence. Relevant ESG topics, such as water and biodiversity footprint, can be linked to existing forecasting tools in controlling and thus the monitoring of progress and targets is achieved. Together with internal reporting to the board level, this is a central control function within the company. Taking again the CO2 example, an elementary part of the strategic and financial planning process must be the incorporation of the cost and revenue effects from the planned carbon emissions of the business model. Considering scenarios for the CO2 price range and the amount of carbon emissions in the coming years is a best practice example to design the net-zero transformation in the most value-creating way and timing.

The same can be said for the accounting and investor relations departments, as they are responsible for external reporting on all relevant ESG topics, goals, and strategies. In cooperation with the treasury department, better financing conditions can be achieved on the capital market, or ESG-linked financing instruments can be set up together with key account banks.

In addition, M&A departments can make use of sustainability aspects as key criteria for their current and future investment activities. A stringent investment strategy can be a powerful approach to buy and separate companies into a corporate structure to bundle “green” business models as well as a bundle of “black” business models. This speeds up the strategic and sustainable transformation by acquiring companies that help to complete the own future net-zero business model and by divesting from expiring business models and stranded assets, inevitably linked to very high carbon emissions. Examples of this pattern include Continental with its powertrain business and Mann+Hummel’s high-performance plastic products, but can be found all over the different industries. Such carve-outs, like a focus on green (and black) business model strategies and transparent capital allocation options, are accelerating strategic change.

Last but not least, for risk management, the embedding of ESG risks and opportunities into existing risk monitoring processes helps to identify physical and transformative risks faster and more reliably.

Focus must be set on business-critical ESG issues

Topics that are crucial for integrated ESG management must be identified from a wide range of sustainability topics. Doing this from the perspective of a materiality analysis, as part of the ESG reporting framework CSRD (Corporate Sustainability Reporting Directive), is insufficient as the key is to focus on actual financial relevance for a company. It is instead recommended to use the following two dimensions.

First, the dimension of regulatory and compliance, especially those that impose financially relevant constrains on current business models and operations. These include, for example, a 1.5 °C alignment under the Science Based Targets initiative,8 the alignment with EU Taxonomy9 classification of sustainable businesses, industry-specific regulations such as the European Battery Regulation10 or the Circular Economy Action Plan,11 the forthcoming Corporate Sustainability Due Diligence Directive12 (CSDDD) and Carbon Border Adjustment Mechanism13 (CBAM), but capital market ESG ratings might be considered relevant as well.

Second, the perspective of current and future business risks and opportunities arising from operating in a global marketplace driven by sustainability and crossing global natural resource boundaries. These include physical risks from climate change, transformative risks from business models that become obsolete, opportunities from new emerging profit pools in or on the way to a net-zero environment, supply chain risks from emerging markets, and rising fossil fuel energy costs from CO2 prices.

Thereby identified topics are to be considered important to the CFO and corporate finance functions if they impact business strategy, mitigate transformative or physical risks, are aspects of upcoming legislations, or have a direct impact on the company's profit or cost base.

Being resilient within the sustainability transformation quickly becomes a corporate advantage worth aiming for

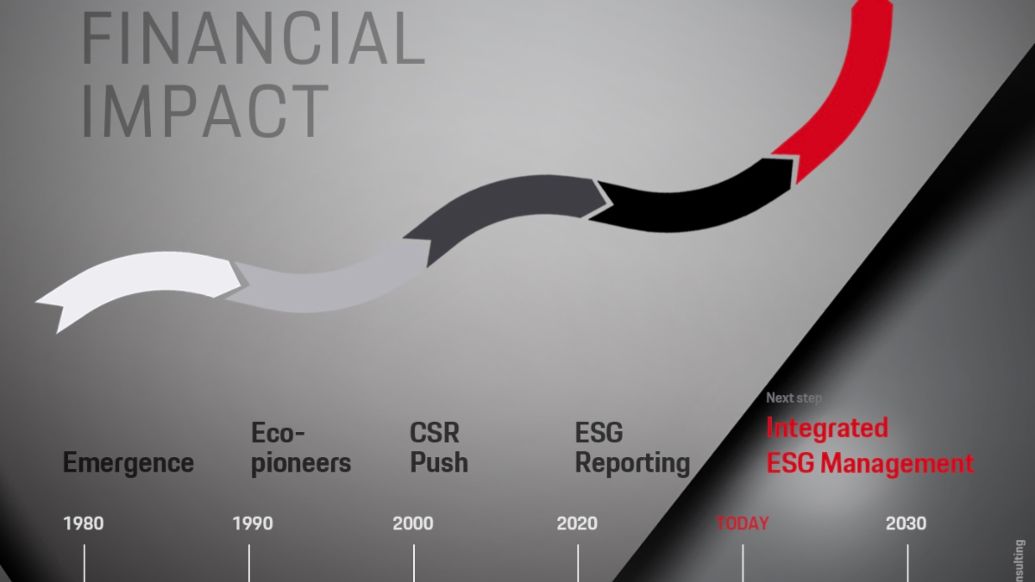

The fact that carbon emissions will be a driver of corporate financial performance in the coming years may seem plausible today, but it was not so just a few years ago. Similar conclusions must be drawn for other ESG issues that have gained dramatic momentum in recent years. Already today, water consumption and scarcity or loss of biodiversity are real threats to industries and therefore need to be considered. The same is true for supply of raw materials and recycled materials, as availability will become even more limited. Thus, future price increases caused by today's pollution and consumption must be taken into account — and CFOs are well-advised to include considerations in the financial agenda.

So why shouldn’t it be done? It may seem complex and unpredictable at first glance, but if you look back at early climate predictions, one finds the deviation from today’s reality is rather small.14 Similar conclusions should be drawn when it comes to other planetary limitations15 for a globalized economy. Linking financial decisions to the price of sustainability is not a limitation towards certain business models but rather an empowerment of CFOs and their board members to make decisions in favor of the future of their company.

Key takeaways

- Sustainability risks and challenges can be modelled such that financial implications for current operations and businesses can be concluded.

- All business-relevant sustainability topics need to be integrated into existing CFO functions via ESG management, consisting of monitoring, analysis, and steering instruments.

- Only a limited set of sustainability topics directly influences a corporate top or bottom line; consequently, ESG steering must be done separately from reporting frameworks.

Info

Text first published in Porsche Consulting Magazine.

Authors: Dr. Tim Dereymaeker, Dr. Philipp Schaller, Dr. Andreas Schreiber